#include <boost/math/distributions/normal.hpp>

namespace boost{ namespace math{

template <class RealType = double,

class Policy = policies::policy<> >

class normal_distribution;

typedef normal_distribution<> normal;

template <class RealType, class Policy>

class normal_distribution

{

public:

typedef RealType value_type;

typedef Policy policy_type;

normal_distribution(RealType mean = 0, RealType sd = 1);

RealType mean()const; RealType standard_deviation()const; RealType location()const;

RealType scale()const;

};

}}

The normal distribution is probably the most well known statistical distribution:

it is also known as the Gaussian Distribution. A normal distribution

with mean zero and standard deviation one is known as the Standard

Normal Distribution.

Given mean μ and standard deviation σ it has the PDF:

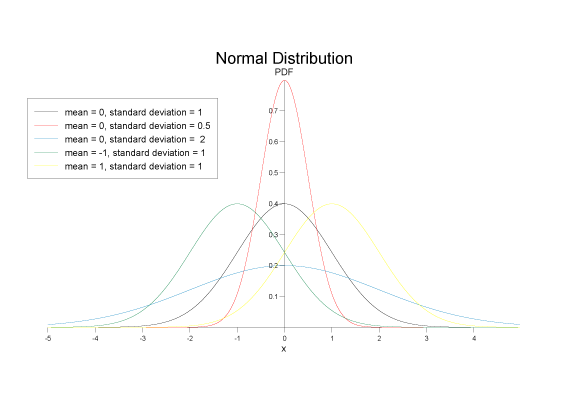

The variation the PDF with its parameters is illustrated in the following

graph:

normal_distribution(RealType mean = 0, RealType sd = 1);

Constructs a normal distribution with mean mean

and standard deviation sd.

Requires sd > 0, otherwise domain_error

is called.

RealType mean()const;

RealType location()const;

both return the mean of this distribution.

RealType standard_deviation()const;

RealType scale()const;

both return the standard deviation of this distribution.

(Redundant location and scale function are provided to match other similar

distributions, allowing the functions find_location and find_scale to

be used generically).

All the usual non-member

accessor functions that are generic to all distributions are supported:

Cumulative Distribution Function,

Probability Density Function, Quantile, Hazard

Function, Cumulative Hazard Function,

mean, median,

mode, variance,

standard deviation, skewness,

kurtosis, kurtosis_excess,

range and support.

The domain of the random variable is [-[max_value], +[min_value]]. However,

the pdf of +∞ and -∞ = 0 is also supported, and cdf at -∞ = 0, cdf at +∞ = 1,

and complement cdf -∞ = 1 and +∞ = 0, if RealType permits.

The normal distribution is implemented in terms of the error

function, and as such should have very low error rates.

In the following table m is the mean of the distribution,

and s is its standard deviation.

Boost

C++ Libraries

Boost

C++ Libraries